Introduction

Cryptocurrency has rapidly evolved from a niche digital experiment into a foundational global asset class. However, as the ecosystem matures and attracts institutional capital, so does the intensity of regulatory oversight. If you have bought, sold, swapped, or earned digital assets during the year, preparing a comprehensive crypto tax return is no longer just a best practice—it is an absolute legal necessity.

With the Internal Revenue Service (IRS) and international tax authorities drastically tightening their grip through new compliance frameworks, including the rollout of Form 1099-DA and strict per-wallet tracking rules, filing an accurate crypto tax return has become inherently more complex. Ignoring your digital footprint or relying on guesswork can lead to steep financial penalties, interest on unpaid amounts, or even intensive audits.

Pro Tip: Your crypto tax return must accurately reflect all global transactions, including off-shore exchanges and decentralized finance (DeFi) activity. Tax agencies now utilize advanced data-matching algorithms to pinpoint discrepancies between broker-reported data and taxpayer filings.

This guide provides a comprehensive, step-by-step approach to filing your crypto tax return. Whether you are a casual investor accumulating assets or a high-frequency algorithmic trader, we will cover everything from foundational tax classifications and strategic trading methodologies to navigating the absolute latest regulatory updates.

Understanding Crypto Taxation: Capital Gains vs. Income

Before you can effectively file your crypto tax return, you must understand exactly how digital assets are classified. In the United States and the majority of developed jurisdictions, cryptocurrency is treated as property for tax purposes, not as fiat currency. This means every taxable event generally falls into one of two distinct categories: capital gains or ordinary income.

Capital Gains

A capital gain (or loss) occurs when you dispose of a cryptocurrency. The IRS tracks the moment you relinquish control of an asset in exchange for measurable value. Common disposal events include: * Selling cryptocurrency for fiat currency (e.g., cashing out Bitcoin to USD or EUR). * Trading one cryptocurrency directly for another (e.g., swapping Ethereum for Solana). * Using digital assets to purchase real-world goods or services.

The specific amount of tax you owe on your capital gains depends entirely on your holding period—how long you maintained ownership of the asset before disposing of it: * Short-Term Capital Gains: Assets held for 12 months or less are taxed at your ordinary income tax rate. In the U.S., these rates currently range from 10% to 37%, depending on your overall income bracket. * Long-Term Capital Gains: Assets held for more than 12 months benefit from significantly reduced, preferential tax rates. These are taxed at 0%, 15%, or 20%, heavily incentivizing a buy-and-hold strategy.

Ordinary Income

Certain cryptocurrency activities do not involve selling an asset but rather earning new assets. These activities generate ordinary income, meaning the fair market value of the cryptocurrency at the exact time of receipt is taxed according to your regular income tax bracket. Income events include: * Earning staking rewards, liquidity provider fees, or yield farming interest. * Receiving unpredictable airdrops or hard fork coins. * Getting paid in cryptocurrency for a job, freelance work, or rendering professional services. * Mining cryptocurrency via Proof-of-Work hardware.

Tax Event Comparison Table

| Transaction Type | Tax Classification | Example Scenario |

|---|---|---|

| Selling Bitcoin for USD | Capital Gains | Selling 1 BTC to cash out fiat directly to your bank account. |

| Trading ETH for SOL | Capital Gains | Swapping Ethereum for Solana on a decentralized exchange. |

| Buying a laptop with LTC | Capital Gains | Using a crypto debit card to pay for daily consumer expenses. |

| Staking ADA on a validator | Ordinary Income | Receiving weekly Cardano staking rewards directly in your wallet. |

| Receiving a Protocol Airdrop | Ordinary Income | Claiming free governance tokens distributed to active protocol users. |

| Transferring to self-custody | Non-Taxable | Moving assets safely from an exchange to a hardware wallet. |

The Role of Trading Strategies in Crypto Taxes

For active participants in the financial markets, the specific trading strategy you employ directly impacts the ultimate complexity and liability of your crypto tax return. Astute investors use various calculated methodologies to legally minimize their tax burden.

Tax-Loss Harvesting

Tax-loss harvesting is a fundamental and powerful strategy for offsetting capital gains. If you sell a cryptocurrency at a loss, you can explicitly use that loss to cancel out capital gains realized from other highly profitable trades.

If your total losses happen to exceed your combined gains for the year, the IRS allows you to deduct up to $3,000 of net capital losses against your ordinary personal income. Any remaining losses beyond that $3,000 limit are not wasted; they are carried over indefinitely into future tax years. Since the traditional wash sale rule has historically not applied to digital assets in the same strict manner as stock equities, crypto traders frequently harvest losses during market dips to optimize their end-of-year crypto tax return.

Accounting Methods: FIFO vs. Specific Identification

The specific accounting method you use to calculate your cost basis ultimately determines your exact taxable gain. Historically, taxpayers had the freedom to choose between Highest In, First Out (HIFO), Last In, First Out (LIFO), and First In, First Out (FIFO). By carefully choosing specific identification methods like HIFO, savvy traders could minimize their recognizable gains by legitimately claiming they sold the most expensive tokens first.

However, recent regulatory shifts demand much more rigorous tracking. Under new government guidelines, standardizing on FIFO or maintaining meticulous, per-wallet specific unit allocation (as explicitly outlined in IRS Revenue Procedure 2024-28) is essential. If you fail to keep completely adequate transaction records, tax authorities will automatically default your accounting method to FIFO. This default could result in significantly higher taxes if you are forced to liquidate early, low-cost baseline investments.

Technical Analysis and Timing Your Tax Events

While technical analysis (TA) is primarily utilized by traders for identifying market entry and exit points, it is also surprisingly relevant for high-level tax planning. By aligning your chart analysis with your asset holding periods, you can make incredibly tax-efficient decisions.

Aligning Exits with Long-Term Capital Gains

Imagine a swing trader utilizing moving average crossovers and Relative Strength Index (RSI) metrics to identify a macro bullish trend. If the technical indicators strongly suggest a major rally is approaching its terminal peak, the trader must urgently check their portfolio holding periods.

If an asset has been held for 11 months, the trader might intelligently decide to hold off on selling for another four weeks, braving potential short-term volatility to safely transition the asset into the long-term capital gains bracket. A slight drop in the asset's price during that extra month might be mathematically offset by the substantial reduction in the tax rate (for example, effectively dropping from a 37% short-term rate down to a 15% or 20% long-term rate).

Using Support Levels for Harvesting

Conversely, when the broader digital asset market aggressively corrects, technical analysts constantly look for key support levels. If a speculative altcoin firmly breaks below strong historical support and enters a prolonged, undeniable downtrend, a trader can use this specific technical breakdown as an immediate trigger for tax-loss harvesting. They can confidently sell the asset to realize the paper loss for their crypto tax return, and subsequently reallocate the preserved capital into a stronger asset showing relative strength on the daily charts.

Navigating New Reporting Requirements: Form 1099-DA

The institutional landscape of digital asset reporting has been completely transformed. If you use centralized trading exchanges, your crypto tax return is now heavily influenced by the implementation of Form 1099-DA (Digital Asset Proceeds from Broker Transactions).

Understanding Form 1099-DA

Designed primarily to close the massive tax compliance gap, Form 1099-DA forces digital asset brokers, exchanges, and custodial payment processors to actively report user transaction activity directly to the IRS. For its initial implementation phase covering the 2025 tax year (filed in 2026), this standardized form primarily reports gross proceeds.

This fundamentally means the IRS sees the total, raw dollar amount of every single crypto sale you executed, but they do not necessarily see your original purchase price (your true cost basis). If your Form 1099-DA reports $100,000 in gross proceeds, the IRS matching system will essentially assume you have $100,000 in purely taxable capital gains unless you proactively file your crypto tax return and explicitly prove your actual cost basis. If you originally bought that crypto for $90,000, you legally only owe taxes on the $10,000 profit. Failing to report the actual cost basis via your proper tax forms will unequivocally lead to heavily inflated tax bills and automated IRS warning notices.

The Per-Wallet Tracking Standard

To add to the overarching compliance complexity, the IRS recently introduced mandatory per-wallet tracking rules. Taxpayers are no longer permitted to loosely aggregate their digital holdings in a single, massive universal pool. Instead, gains, losses, and precise cost bases must be tracked meticulously on a wallet-by-wallet or individual account-by-account basis. This stringent requirement makes using automated accounting software critical, as manually calculating cross-chain cost basis across decentralized exchanges, cold storage hardware wallets, and centralized custodial platforms is nearly impossible without computational help.

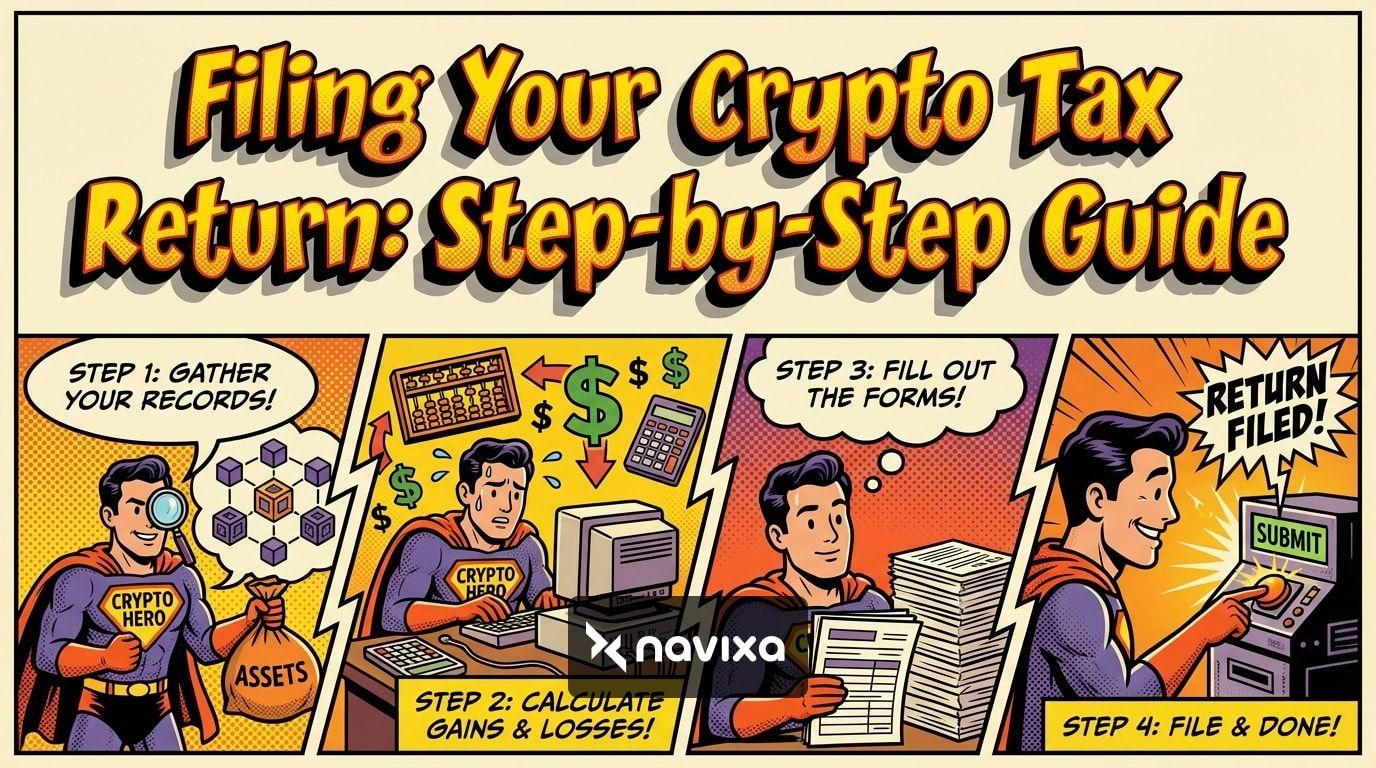

Actionable Steps to File Your Crypto Tax Return

Preparing your official tax filing doesn't have to be an overwhelming ordeal. Follow these actionable, step-by-step instructions to ensure maximum accuracy and absolute compliance.

Step 1: Gather All Transaction Records

You must compile a perfectly complete history of all your crypto activities across every single platform you have ever interacted with. This mandatory collection phase includes: * Exporting CSV files and complete transaction histories from centralized exchanges. * Copying your public wallet addresses for all on-chain activities (DeFi swaps, NFT trades, blockchain staking). * Compiling records of over-the-counter (OTC) trades or private peer-to-peer transactions. * Locating all official Form 1099-DA statements received directly from your connected brokers.

Step 2: Use Crypto Tax Software

Because of the aforementioned per-wallet tracking rules and the sheer, overwhelming volume of daily micro-transactions (like network gas fees), utilizing specialized tax software is strongly recommended. Platforms like CoinTracker or Koinly securely sync via read-only APIs to your various exchange accounts and public blockchain addresses. They will automatically classify complex transfers, algorithmically match your historical cost basis, and instantly calculate your true capital gains and ordinary income.

Step 3: Reconcile Missing Cost Basis

The most notoriously common error when preparing a crypto tax return is the missing cost basis problem. This typically happens when you buy an asset on Platform A and transfer it over to Platform B to ultimately sell. Platform B inherently doesn't know what you originally paid on Platform A, so your newly generated tax software might improperly assume a $0 cost basis, heavily inflating your perceived taxes. Take the requisite time to manually reconcile these specific transfers so the software properly connects the original fiat purchase to the eventual sale.

Step 4: Complete the Necessary Tax Forms

If you are a U.S. taxpayer, formally finalizing your crypto activity will generally require the completion of the following crucial forms: * Form 8949 (Sales and Other Dispositions of Capital Assets): Extensively used to list every individual taxable crypto disposal, strictly including the date acquired, the date sold, gross proceeds, and total cost basis. * Schedule D: Directly summarizes your total, aggregated capital gains and losses pulled from Form 8949. * Schedule 1 (Form 1040): Specifically used to report your total ordinary income acquired from protocol airdrops, validator staking, or network hard forks. * Form 1040: Do not forget to affirmatively check the Digital Assets box on the main front page of your tax return, explicitly indicating whether you received, sold, or otherwise interacted with cryptocurrency during the tax year.

Risk Management and Audit Defense

In the fast-paced realm of crypto trading, risk management usually refers to strict stop-loss orders and balanced portfolio sizing. However, proactive tax compliance is an equally vital, yet often ignored, component of financial risk management.

The IRS and similar international authorities utilize highly advanced data-matching algorithms to instantly cross-reference the 1099-DA forms they receive from exchanges with the individual crypto tax return you ultimately file. Discrepancies are flagged automatically. To vigorously defend yourself against potential tax audits: 1. Maintain Meticulous Records: Keep secure, digital copies of all CSV files, linked wallet addresses, and software calculation reports for a minimum of three to five years. 2. Never Ignore a 1099 Form: Even if the broker's 1099-DA undeniably has an internal error, you must publicly acknowledge the gross proceeds on your tax return and make a formal adjustment to accurately reflect the true cost basis. Ignoring the form entirely will instantaneously trigger an automated underreporter inquiry. 3. Consult a Tax Professional: If you actively engage in highly complex DeFi protocols, massive liquidity pooling, or run a crypto-centric enterprise, hire a Certified Public Accountant (CPA) who exclusively specializes in digital assets. You can review further general guidelines directly via the IRS official website.

Practical Takeaways

* Always clearly differentiate between your capital gains (selling/trading assets) and your ordinary income (staking/airdrops). * Proactively leverage strategic tax-loss harvesting before the definitive end of the calendar tax year to massively offset your highly profitable trades. * Strictly implement per-wallet tracking procedures to fully comply with modern IRS requirements and ensure highly accurate, undeniable cost basis calculations. * Do not naively rely solely on broker-issued Form 1099-DA for your final tax prep; utilize specialized crypto tax software to establish your comprehensive, global cost basis and avoid paying unnecessary taxes on mere gross proceeds.

Conclusion

Successfully navigating the labyrinthine complexities of digital asset taxation is a fundamentally vital part of being a highly responsible, legally compliant investor. By deeply understanding how different trading methodologies affect your core liabilities, keeping pristine financial records, and actively utilizing the right automated software, you can confidently file a highly accurate crypto tax return. Don't let new, stringent reporting requirements like the rollout of Form 1099-DA catch your portfolio off guard. Take immediate control of your financial data today, thoroughly streamline your reporting process, and actively consult with a certified crypto tax professional to aggressively optimize your wealth strategy for the profitable years ahead.

Frequently Asked Questions

What happens if I don't file a crypto tax return?

Failing to actively report your taxable cryptocurrency transactions is legally considered tax evasion by the IRS and equivalent global tax authorities. This severe oversight can rapidly lead to massive monetary penalties, compounding interest on all unpaid taxes, and in extreme cases of willful negligence, formal criminal prosecution. With centralized exchanges now proactively reporting your data via mandatory forms like 1099-DA, tax authorities already know you traded—it is your absolute responsibility to properly reconcile the math.

Do I have to pay taxes if I just hold my crypto?

No. Simply buying cryptocurrency with standard fiat currency and passively holding it in an exchange account or personal cold-storage wallet is not a taxable event. Taxes are exclusively triggered upon the active disposal of the asset (selling it for cash, trading it for another coin, or actively spending it) or when you earn completely new assets as classified income (like staking rewards or protocol airdrops).

How do I handle taxes on decentralized exchanges (DeFi)?

DeFi transactions, such as wrapping fundamental tokens, actively providing liquidity to decentralized pools, or anonymously swapping assets on automated platforms like Uniswap, are generally considered taxable events by governing bodies. Because anonymous DeFi platforms do not issue 1099 forms or verify user identities, the legal burden is entirely on the individual taxpayer to intricately track these complex, on-chain activities using highly specialized, read-only crypto tax software.

Can I write off crypto losses?

Yes. If you explicitly sell a cryptocurrency for less monetary value than you originally acquired it for, you realize a capital loss. You can legally use these defined losses to cleanly offset your capital gains realized in the exact same tax year. If your total losses deeply exceed your total gains, U.S. taxpayers can actively deduct up to $3,000 against their ordinary income, smoothly carrying the remainder forward into future consecutive tax years.

What should I do if my 1099-DA is completely incorrect?

Because the initial rollout of Form 1099-DA strictly tracks only gross proceeds and often severely lacks cost basis data from external wallet transfers, the isolated numbers might appear wildly inaccurate or inflated. Do not ignore the official form under any circumstances. You must explicitly report the gross proceeds provided on the form, and then systematically supply your own irrefutable documentation (via IRS Form 8949) to concretely prove your actual cost basis, thereby allowing you to calculate the legally correct net gain or loss.